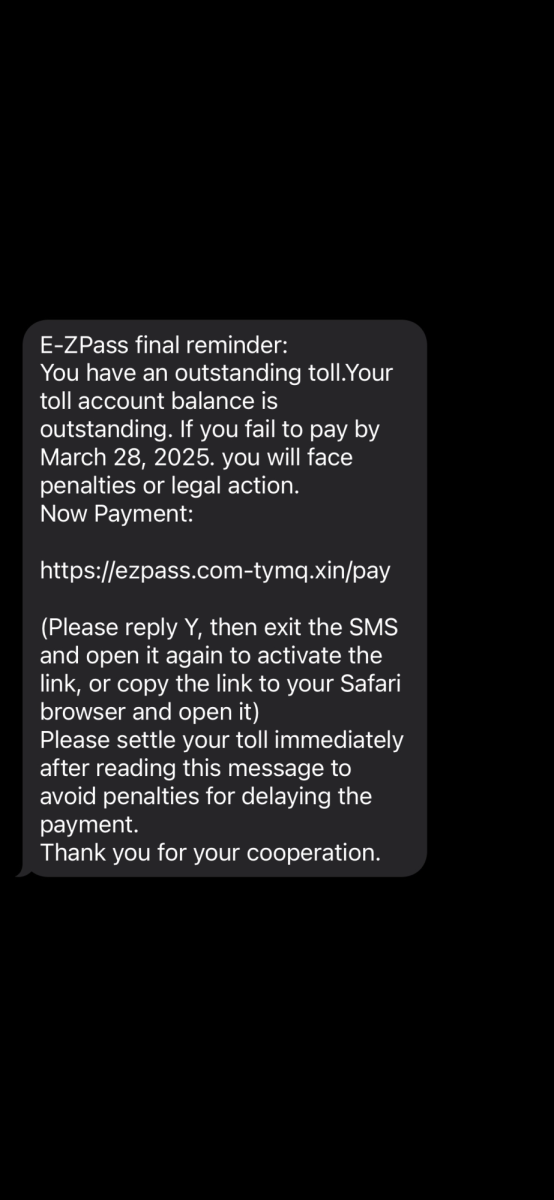

The Consumer Financial Protection Bureau (CFPB) is an agency created due to the 2008 financial crisis to protect consumers from unfair financial practices. On Feb. 10, Budget Director Russell Vought emailed the CFPB staff to notify them to cease work. The shutdown has Americans questioning their protection against predatory actions in the financial services section.

“This could be a major negative event where Americans could potentially lose trust long term in the financial system.” – Mike Ryan, Department head of economics and finance at the University of North Georgia

CFPB was established in 2011 due to the Dodd-Frank Wall Street Reform and Consumer Protection Act, the CFPB was made to be a monitoring agency to ensure that consumers were treated fairly by banks, mortgage companies, credit card firms and other finance companies. This institution has been crucial for enforcing regulations there to encourage transparency and accountability in consumer finance. This allows individuals to make educational decisions about loans, mortgages, and credit.

The closure of CFPB comes at a time when vulnerability is high within Americans, dealing with inflation after the pandemic in 2019 causing economic uncertainty. The agency’s discontinuation causes apprehension about potential increases in fraudulent activity and questionable lending practices. Consumers might find themselves at bigger risk without the companies’ resources to help restore knowledge and help with particular financial hardships.

Ryan discussed the agencies’ importance, saying, “Consumers might not be too financially savvy, and the CFPB will help you with where you need to go and what you can do. They helped consumers contain $18 billion from fraudulent predatory practices.”

The exact reason for the shutting down of the CFPB remains unclear and complex, nearing towards a more political issue involving financial regulation. Although it has been shut down, proponents much like Ryan, believe the company is essential for protecting consumers and holding financial institutions accountable.

The desolate office could encourage unscrupulous lenders and create an environment where deceptive practices become a norm. The end of the CFPB could start a shift in consumer finance, pushing Americans to become more financially literate and take further precautions with their pecuniary matters.